Experiential Investing - Where NFT's & Security Tokens Collide

A collection of thoughts on NFT's vs. securities, and on how these technologies may work together to provide unique experiences for issuers and investors.

By Vertalo Team

All throughout the boom of the NFT craze in 2021 we took phone calls from people who were seeing what was going on and wanted to find a way to use the hype to their advantage. We were a part of many Clubhouse rooms discussing the prospective use-cases for NFT’s in an internet world. NFT issuers like CryptoPunks & the Bored Ape Yacht Club had not only provided incredible collectibles to the marketplace that soared in value (whether one agrees with the valuations is another story altogether), but that also offered their holders unique access to elite events and valuable, if not exclusive, experiences.

Not all of these were actual parties, often times this unique access meant benefits of other kinds, including online communities, access to celebrity figures, or other interesting benefits, but the message was clear: retail investors were interested in NFT’s. The emergence of many different NFT platforms further bolsters this idea, as many fought for marketshare against giant OpenSea, which held north of 90% marketshare at its peak.

A quick anecdote: In 2019 one of the top NBA teams in the country reached out interested in issuing a non-equity incentive token (this was long before NFT’s blew up, mind you) with the idea that they would function as non-equity collectibles with value. One of their ideas was to give the top individual token holder the ability to fly with the team on the jet to away games when the team traveled as a tokenholder perk. With the benefit of hindsight, we can confidently say that their creativity, experience design, and out-of-the-box thinking was quite impressive and well ahead of its time. We wish they’d gone forward with their ideas.

Beyond those only seeking profits, the driver for many throughout this was a theme we see over and over as companies seek to build brand loyalty and stand out amongst competitors creating similar products without real lines of differentiation. Community and those willing to support brands and companies will always be highly valuable. And while we don’t agree with marketers that tout brand/human relationships as synonymous with human/human relationships, we certainly believe in the power of word of mouth advertising, and that brands have the ability to create more lasting revenue streams when they fully convert their users into evangelizers.

For example, we use several apps for automating savings and recurring investments. We’ve come to enjoy their products so much we recommend them to our family and friends, and even colleagues at the office. One member of our team helped their sister get set up an automated savings plan (which netted them $5 for the referral!) and she has since used it to help cover business expenses and go on a vacation. We’re raving fans of these apps, and Iwe have over a dozen folks we’ve recommended them to that prove it.

We can learn a lesson from the NFT market and craze that popped off in 2021:

Brand loyalty, when well executed, can be a force multiplier for your business, products, and revenues.

What are NFT’s?

We’ll keep this brief since there are many resources online for these sort of questions; NFT’s are cryptographic blockchain tokens, similar to security tokens or other cryptocurrencies, except they are serialized, designed to function as one-of-one or one-of-many (in the case of collections), while still maintaining unique and individual properties at the token level. A great graphic from OpenSea highlights the differences between token types:

Can NFT’s be used for security tokens?

The real question on the table - can we use a serialized blockchain-bound cryptographic token for a security?

In a single word, no.

NFT’s are incompatible with securitization as we know it today.

Fungibility is an important characteristic when considering how markets behave, and certainly where currencies are considered. If you have a dollar, and your friend has a dollar, and you trade dollars, no value has changed hands. That’s a feature, not a bug, and a core requirement for modern financial systems. Different classes of dollars with different features would be chaotic, even if there could be interesting and stimulating implications of such a system (imagining something akin to foreign exchange markets, but within a single jurisdiction).

To be clear, We are staunch believers in competition, especially Murray Rothbard’s theory of competing currencies, as detailed in his forward book, “What Has Government Done to Our Money?” and would love to see more competing currency options as adoption of blockchain grows. That said, a government issuing multiple classes of currencies could be problematic, for example, when the Romans used copper, silver, & gold as legal tender, which immediately led to Gresham’s Law, where good money is hoarded and bad money is used precisely because it is less valuable and/or scarce, and therefore unappealing as a store of value.

Nearly all of the shares you could buy of public companies on a brokerage today are common shares. They are fungible one with another, subject to a single CUSIP or ISIN number for identification, in support of the settlement and clearing process.

To be fair, many companies do use a dual-class structure, that gives more voting rights to the board of directors and/or c-suite of executives, but when we’re talking about purchasable shares from your brokerage, you’re buying shares that are fungible one with another. This is a feature where a high number of shares outstanding is concerned.

We recently came across an interesting take that said something along these lines, “NFT’s are simply an interface, replace ‘NFT’ with ‘row in excel’ and you’ll get the general idea.” While we like the simplicity of the analogy, it inadvertently displays the problem with using NFT’s as securities: if each “row in excel” is unique to itself, then a Securities Information Processor or the DTCC would have to track each one individually. You’re theoretically talking about amplifying billions of transactions by thousands of times. If anyone wants to pitch this to the DTCC, please call us when you do, we’d love to hear their reaction to that proposal.

A brief note on conflating token types

Depending on the utility of the NFT used, there may be hazards in conflating token types, whether it’s NFT’s as securities or utilities as a payment medium. One unique example we can think of is when Gucci announced they had added the Bored Ape Yacht Club’s native token, ApeCoin, as a payment method for their products. On paper this is extremely cool, since we’re seeing the convergence of several things here:

Staking tokens

NFT community

NFT utility, and

Payment rails

But let’s dig a little deeper and see if we can’t uncover any problems this partnership might represent. There’s a reason why most require you to take assets and settle to cash first, rather than pay with the asset itself, and it comes to down to proper asset handling, as well as tax implications. Typically you don’t use the deed to an asset as payment, but rather sell the asset, and use cash for payment.

In order to properly handle ApeCoin as a payment medium, Gucci enlisted the help of BitPay, one of the world’s foremost crypto payment processors. We’ve seen BitPay’s product and have been impressed with their breadth of services, including their Payment Services, BitPay Send (which allows for users to disburse crypto to registered users), and others.

Side note: In order to properly account for AML risks with their Send product, BitPay applies on-chain analytics, machine learning, and AI to constantly assess for risk and compliance hazards. Since blockchain wallets are pseudonymous, this is a very unique, albeit solvable, challenge, where securities are involved.

Now, having demoed BitPay’s product, we know that they have internal mechanisms that they offer to users, including the ability to reduce counterparty risk where the crypto or network itself is concerned. If we used crypto to pay for a product, but the network activity was very high, there may be a slight difference in terms of the value paid in, in real USD terms, once the payment is processed and hits the end user’s account.

For example, a cursory look at Gucci’s website shows this Wool cashmere formal jacket clocking in at just under $5,000.00. With how volatile crypto can be, if network fees were high and we used ApeCoin to pay for this item, if the price of ApeCoin dipped 50-100 bps (which unfortunately is not unrealistic in the crypto world), Gucci may have just offered us a discount unintentionally. In order to offset this risk with crypto as a payment tool, upon receiving payment, BitPay will benchmark and peg the USD equivalent value of the paid-in crypto for 15 minutes, allowing the issuer to automate a conversion from ApeCoin into USDC or US dollars directly, without being worried that the value of ApeCoin could dip, leading to the aforementioned unintentional discount.

Regarding Centralization. Another hazard, although admittedly one that doesn’t matter when considering NFT’s vs. securities, is that of centralization. ApeCoin (ERC20 native standard) was designed as a voting and governance token, giving holders say in the future of the community, including development projects and resource allocation. If Gucci, through enabling ApeCoin as a payment medium and not a mere governance token, starting gathering ApeCoin they could easily amass enough to subvert the community and control minority voting rights. After all, 64% of all staked ETH is controlled by just 5 entities. The same could be said of BitPay, depending on how the payment processing worked per the party accepting ApeCoin as legal tender, BitPay could begin hoarding ApeCoin for whatever purposes they wanted to.

Serializing securities serves no purpose

We’ve thought long and hard about this, especially during the NFT boom as we were fielding interest from many different parties, and are open to being proven wrong if you disagree, but we simply don’t see the value of using an NFT protocol to issue securities. In fact, we only think could yield problems for issuers, investors, regulated actors, and the market at large.

Let’s review some of the reasons why using NFT’s as securities would be problematic:

Securities should be fungible

Securities that freely trade are designed to be fungible one with another, whether its for voting, dividend distribution, derivatives, or a simple buy-and-hold position. The creation of non-fungible instruments would be akin to creating a unique share class for each and every asset. Lot-level tracking, for tax and accounting purposes, is certainly necessary, but the creation of hundreds or thousands of asset classes? That simply introduces unnecessary complexity into an already complex process.

Where NFT’s could be used to represent titles, we see an incredible use-case long term, from mortgages to employment contracts, auto leases to credit cards, lending agreements to voting in elections, we think the disruptive capability NFT technology represents in our world today is quite literally immeasurable. But it’s a poor take to assume that serializing securities would add any utility or functional purpose where fungible securities are required.

With on-chain digital asset securities, you can track the history of the stock you hold

While this seems obvious, we state this based on conversations we’ve had amid misunderstandings of security tokenization: the tracking of the history of a blockchain-based token does not require an NFT implementation.

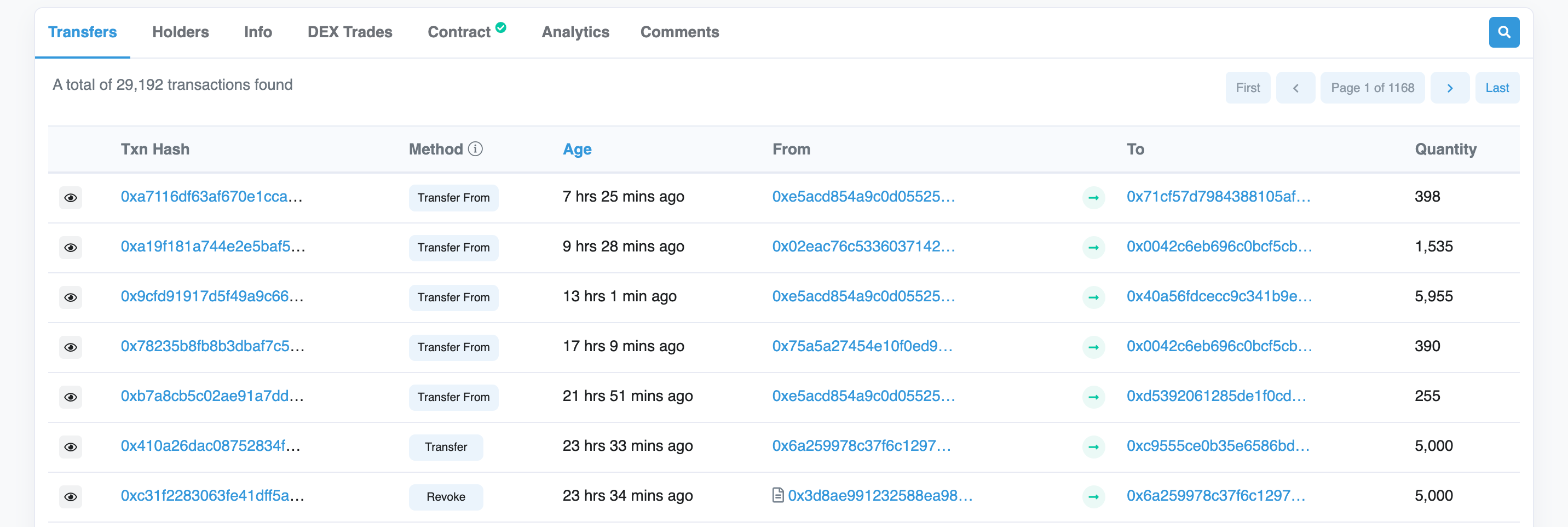

Indeed, one of the premier benefits of using blockchain for securities is the historicity and transparency that public blockchains offer. A quick look at Etherscan under an ERC1404 standard contract (a common digital asset securities protocol that maintains compliance in most regulated jurisdictions) gives us insights into transfers from, transfers to, number of units, the transaction hash, and even the type of transfer denoted under “Method”.

Serialized securities serve no functional purpose

As mentioned previously, you may as well create 500 unique classes of stock, since if they aren’t fungible - each and every token is different. If you’re talking about artwork, collectibles, or other unique assets (think collectible guitars or supercars), this non-fungibility is valuable, but where securities are concerned, it would radically complicate the issuance, cap table management, and secondary trading processes. When Vertalo worked with XY Labs to digitize and transform their cap table, a core part of this process was to collapse all existing shares down into a single common stock share class that could support free trading.

Most NFT protocols do not address securities regulations

This is a surface level challenge, since adding either serialization to an existing securities protocol, or a control function to an existing NFT protocol, would be in theory relatively straightforward, but the most dominant NFT protocols currently do not address the requisite treatment of the tokens as securities. For example, ERC-721 is the most common NFT issuance protocol, and it does have certain control provisions, especially the safeTransferFrom method, which guarantees the address it’s being sent to can properly receive and handle the NFT itself.

function safeTransferFrom(address _from, address _to, uint256 _tokenId) external payable;

/// @notice Transfer ownership of an NFT -- THE CALLER IS RESPONSIBLE

/// TO CONFIRM THAT `_to` IS CAPABLE OF RECEIVING NFTS OR ELSE

/// THEY MAY BE PERMANENTLY LOST

/// @dev Throws unless `msg.sender` is the current owner, an authorized

/// operator, or the approved address for this NFT. Throws if `_from` is

/// not the current owner. Throws if `_to` is the zero address. Throws if

/// `_tokenId` is not a valid NFT.

/// @param _from The current owner of the NFT

/// @param _to The new owner

/// @param _tokenId The NFT to transferHowever, the standard transfer method used for ERC-20 tokens is applied here, meaning these are treated as sovereign instruments that can be transferred, staked, sold, or otherwise acted upon at the sole behest of the holder. This also means they could be lost, to an irrecoverable trade or lost wallet scenario. And where securities are concerned, this opens up many problematic scenarios and stands in direct violation with existing regulations. See The Case Against Bearer Assets (as Securities) for more details around the proper treatment of digital asset, or digitally enhanced, securities.

All told, serializing securities would create far more problems than it would bring benefits to issuers, brokers, transfer agents, custodians, and other market participants. In the current capital markets structure we operate in, it simply doesn’t make economic or functional sense to serialize each share of stock in an offering.

Experiential Investing - a new opportunity for security tokens & NFT’s

We believe that the securities industry could learn a lot from the community building and investor support aspects that many of the successful NFT projects have built. As those who have worked in high growth startups can tell you, word-of-mouth advertising is always more valuable than any purchased media or advertising messaging. Hence the importance and emphasis placed the famed “Net Promoter Score,” particularly at businesses with an ongoing relationship with their customers.

The easiest implementation of this would be to simply use the security token the same way NFT projects do. The wallet holding the token could sign a transaction and allow the holder access since they’ve proved they’re a member of the “shareholder club”.

But remember, securities can’t be traded as freely as NFT’s trade on a collectibles marketplace like OpenSea or Rarible, due to the regulatory frameworks around trading securities. This brings us back to one of the core differences between NFT’s and security tokens: a highly liquid market.

Blockchain-based securities are still in their infancy. Nearly all private investments are subject to lockup periods or other restrictions, and all securities must undergo vetting and due diligence before they can be available for secondary trading, which means that securities can’t compete in terms of velocity or depth when it comes to the available liquidity for NFT’s. The liquid market for security tokens is positively dwarfed by the volume and market for collectibles, both traditional and digital. Our hope is that the market for security tokens is the tortoise, whereas the NFT market is the hare, and that eventually the slow-and-steady growth of the security token market matures in the way we envision.

What about a dual offering?

Another approach could be to hold a dual offering of sorts, where the purchasers of the security token also receive an NFT as part of the transaction. As long as it’s truly a collectible and not a security masquerading as an NFT, this could potentially drive some of the more appealing community aspects by acting as a digital collectible that also has an immediate market for buying and selling.

We refer to this as “experiential investing” whereby the investor owns an NFT that provides community and other unique perks, as well as its companion security that represent the upside of the issuer and their future as a business. Each compliment one another without crossing the boundaries between collectible assets and equities.

Whether a high volume of liquidity for the offering could be created or not would most likely come down to the marketing efforts of the issuer and holders of the NFT itself, as we’ve seen with some of the more notorious NFT collections today.

One question that arises is whether or not you could promote the NFT as a dual token offering without running afoul of the regulations for the promotion and distribution of securities, which is a highly regulated activity almost exclusively reserved for licensed professionals. We don’t know how favorably regulators might consider this proposition.

That said, a dual structure raises interesting questions in and of itself, most notably, are these irrevocably linked together, or could they be decoupled? Could you create a market for the NFT, as an experiential token, outside of the ownership of the security?

At first glance the NFT half of an offering like this simply looks like a non-equity incentive. We can’t imagine any problem with a dual offering like this provided you’re treating each instrument according to the securities regulations within your jurisdiction. However, using a collectible side-by-side approach like this could be interesting in driving adoption of the security itself, especially if they were decoupled, but still peripherally related. Should one undertake this, we imagine running KYC and source-of-funds checks on the purchases for both tokens would be prudent, as additional cover where anti-money laundering regulations are concerned.

Another question we have is what would a highly liquid collectible market do for the security itself? Would it drive adoption, if they were linked, or would an initial linking followed by a decoupling and standalone market provide interest and activity a la the security itself?

An often-overlooked, but important driver in the growth of the crypto economy was when venture capital poured into crypto projects, bolstered by eager VC’s who saw alpha and immediate liquidity windows via the first ICO’s the market offered. If there are new or unique ways to drive adoption, and secondary market liquidity, of these instruments, we would love to explore them.

Conclusion

Treating securities as NFT’s, either through serialization or with an existing NFT protocol would cause a number of issues, and is, from our standpoint, not a winning proposition. That said, a combination NFT / security token hybrid could be an interesting attempt at driving adoption and utility. It raises interesting and potentially fun challenges to solve for, at the intersection of securities regulations, blockchain technology, community, brand-marketing, and even investor psychology.

We’d love to see an enterprising project try to implement some sort of dual structure like this. Particularly we’d like to see how the market reacts, what appetite there is for an offering like this, and what technical requirements it would take to perform it properly. But until that happens it’s just some out-loud thinking on our part. Please feel free to comment on the questions raised here, or reach out to us directly if you want to dig in deeper. Despite all that’s happened, there’s still a lot of creativity and development yet to happen in this space.

Till next time.

Interested in connecting over the digital asset ecosystem, capital markets, or blockchain-based securities? Reach out to us on LinkedIn or Twitter!

Disclaimer: We are not attorneys, broker-dealers, investment advisors, or wealth advisors. Nothing presented herein is nor should it be considered as legal, professional, business, investment, or any other kind of advice. The information presented here is done so for educational, informational, and entertainment purposes only. Always consult a licensed professional before taking professional, investment, or legal action.